Section 5: Factors affecting options pricing

Factors affecting options pricing (underlying price, volatility, time, interest rates)

BEGINNER LEVEL

10/6/20258 min read

Key Factors Affecting Options Pricing:

While intrinsic and extrinsic value are the components, several external factors cause these values to change. These are the main drivers of an option's premium:

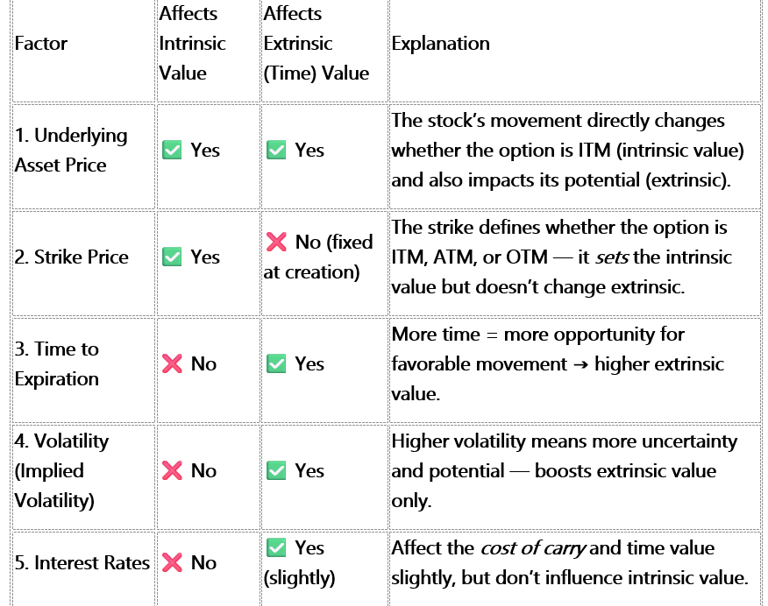

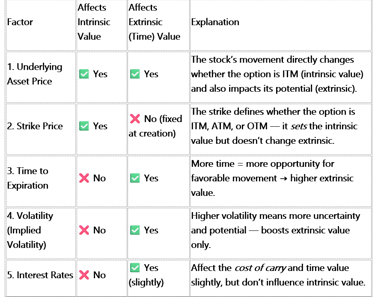

1. Underlying Asset Price: The Engine That Drives It All1

💡 What It Means:

Impact: This is the most direct and powerful factor. As the stock price moves, the option's intrinsic value changes (if it has any), and its extrinsic value is also affected.

Relationship:

Calls: Increase in value as the underlying stock price goes up.

Puts: Increase in value as the underlying stock price goes down.

Think: If a call option gives you the right to buy stock at $50, and the stock jumps to $60, that right is clearly more valuable.

Example:

You own a Call on Apple (AAPL) with a strike price of $180.

If AAPL rises from $180 → $190, your call becomes $10 In-The-Money, and its price might jump from $5 to $11.

But if AAPL drops to $170, your call may lose almost all its value.

🧠 Real-Life Analogy:

Think of your option like a movie ticket.

If the movie (the stock) becomes a blockbuster hit (price rises), everyone wants your ticket — it becomes valuable!

But if the movie flops (price drops), no one wants to buy it from you.2. Strike Price: The Value Gatekeeper

Impact: Directly determines an option's moneyness whether it’s In-The-Money (ITM), At-The-Money (ATM), or Out-of-The-Money (OTM).

That directly affects how much intrinsic valueit has Relationship:

Calls: Lower strike prices (more ITM) have higher premiums.

Puts: Higher strike prices (more ITM) have higher premiums.

Think: A call with a $50 strike on a $55 stock is more valuable than a call with a $60 strike, because the $50 strike is already profitable.

Example:

Imagine two Calls on Microsoft (MSFT):

$300 strike Call (stock = $320) → already profitable → costs $22

$340 strike Call (stock = $320) → not yet profitable → costs only $5

The difference? The first one already has real value, while the second one only has potential.

🧠 Real-Life Analogy:

It’s like having a discount coupon:

One coupon lets you buy shoes for $300 when they cost $320 (you’re already saving — real value!)

Another coupon lets you buy them for $340 — still above today’s price, so it’s only valuable if prices go up later.

3. Time to Expiration: The Countdown Clock (⏳)

Impact: The more time an option has before it expires, the more valuable it is — because there’s more chance the stock might move in your favor.

This added time adds to the extrinsic value.Relationship: Options with more time until expiration are generally more expensive (higher premiums) than options with less time, all else being equal.

Think: An option that expires tomorrow has very little time to make a big move, so its potential is much lower than one that expires in 6 months.

Example:

Two Amazon (AMZN) $150 Calls:

Expires tomorrow: priced at $1.50

Expires in 6 months: priced at $10.00

Both have the same strike and stock price — but one gives you half a year for things to happen, while the other gives you just one night!

🧠 Real-Life Analogy:

Buying more time is like paying rent for an apartment.

A one-night stay is cheap, but renting for six months costs a lot more — you’re paying for the flexibility of time.

In options, time = opportunity, and opportunity costs money.

4. Volatility: The Measure of Uncertainty (⚡)

Impact: Volatility measures how much a stock’s price is expected to move — up or down.

If a stock tends to swing wildly, options on it become more expensive because there’s a higher chance of big profits (or losses).We specifically care about Implied Volatility (IV) — the market’s expectation of future movement, not what happened in the past.

Relationship: Higher expected volatility generally leads to higher options premiums for both calls and puts.

Think: If a stock is known to swing wildly, an option on that stock has a greater chance of becoming profitable, so people are willing to pay more for it. Conversely, if a stock rarely moves, the options are less likely to become profitable and are cheaper.

Example:

Stock A moves quietly from $50 → $52 → $51 → $53.

Stock B jumps around wildly from $50 → $60 → $45 → $58.

Even with the same current price, Stock B’s options will cost more — because the potential for profit is bigger.🧠 Real-Life Analogy:

Imagine two friends:

One is calm and predictable (like Stock A).

The other is unpredictable — might surprise you big time (like Stock B).

5. Interest Rates: The Silent Factor (🏦)

Impact: Changes in interest rates have a relatively minor effect on most short-term stock options. They become more noticeable for long-term options (LEAPS).

Relationship:

Calls: Higher interest rates generally lead to slightly higher call premiums.

Puts: Higher interest rates generally lead to slightly lower put premiums.

Think: This is more complex, relating to the cost of holding or borrowing the underlying asset. For now, understand it's a minor factor for typical stock options.

Example:

If rates rise sharply, investors might prefer holding cash instead of buying stock, which slightly pushes Call prices up and Put prices down.

But this effect is minimal for short-term options (like 1–2 months).🧠 Real-Life Analogy:

Think of interest rates like the rent you pay for money.

When rent (interest) is higher, it costs more to own assets (like stocks), so calls get a small boost (since they delay buying), while puts lose a bit of appeal.

🧾 Summary Table

The 5 Key Factors and How They Affect Option Value (Premium)

🎯 Big Takeaway

These five forces work together — like gears in a machine — to shape every option’s price.

Once you understand them, you can predict how your option’s value might move as the market changes.

That’s how you move from guessing → to strategic thinking in options trading.

Key Factors Affecting Options Pricing:

While intrinsic and extrinsic value are the components, several external factors cause these values to change. These are the main drivers of an option's premium:

Underlying Asset Price: The Engine That Drives It All

💡 What It Means:

Impact: This is the most direct and powerful factor. As the stock price moves, the option's intrinsic value changes (if it has any), and its extrinsic value is also affected.

Relationship:

Calls: Increase in value as the underlying stock price goes up.

Puts: Increase in value as the underlying stock price goes down.

Think: If a call option gives you the right to buy stock at $50, and the stock jumps to $60, that right is clearly more valuable.

Example:

You own a Call on Apple (AAPL) with a strike price of $180.

If AAPL rises from $180 → $190, your call becomes $10 In-The-Money, and its price might jump from $5 to $11.

But if AAPL drops to $170, your call may lose almost all its value.

🧠 Real-Life Analogy:

Think of your option like a movie ticket.

If the movie (the stock) becomes a blockbuster hit (price rises), everyone wants your ticket — it becomes valuable!

But if the movie flops (price drops), no one wants to buy it from you.

Strike Price: The Value Gatekeeper

Impact: Directly determines an option's moneyness whether it’s In-The-Money (ITM), At-The-Money (ATM), or Out-of-The-Money (OTM).

That directly affects how much intrinsic valueit has Relationship:

Calls: Lower strike prices (more ITM) have higher premiums.

Puts: Higher strike prices (more ITM) have higher premiums.

Think: A call with a $50 strike on a $55 stock is more valuable than a call with a $60 strike, because the $50 strike is already profitable.

Example:

Imagine two Calls on Microsoft (MSFT):

$300 strike Call (stock = $320) → already profitable → costs $22

$340 strike Call (stock = $320) → not yet profitable → costs only $5

The difference? The first one already has real value, while the second one only has potential.

🧠 Real-Life Analogy:

It’s like having a discount coupon:

One coupon lets you buy shoes for $300 when they cost $320 (you’re already saving — real value!)

Another coupon lets you buy them for $340 — still above today’s price, so it’s only valuable if prices go up later.

Time to Expiration: The Countdown Clock (⏳)

Impact: The more time an option has before it expires, the more valuable it is — because there’s more chance the stock might move in your favor.

This added time adds to the extrinsic value.Relationship: Options with more time until expiration are generally more expensive (higher premiums) than options with less time, all else being equal.

Think: An option that expires tomorrow has very little time to make a big move, so its potential is much lower than one that expires in 6 months.

Example:

Two Amazon (AMZN) $150 Calls:

Expires tomorrow: priced at $1.50

Expires in 6 months: priced at $10.00

Both have the same strike and stock price — but one gives you half a year for things to happen, while the other gives you just one night!

🧠 Real-Life Analogy:

Buying more time is like paying rent for an apartment.

A one-night stay is cheap, but renting for six months costs a lot more — you’re paying for the flexibility of time.

In options, time = opportunity, and opportunity costs money.

Volatility: The Measure of Uncertainty (⚡)

Impact: Volatility measures how much a stock’s price is expected to move — up or down.

If a stock tends to swing wildly, options on it become more expensive because there’s a higher chance of big profits (or losses).We specifically care about Implied Volatility (IV) — the market’s expectation of future movement, not what happened in the past.

Relationship: Higher expected volatility generally leads to higher options premiums for both calls and puts.

Think: If a stock is known to swing wildly, an option on that stock has a greater chance of becoming profitable, so people are willing to pay more for it. Conversely, if a stock rarely moves, the options are less likely to become profitable and are cheaper.

Example:

Stock A moves quietly from $50 → $52 → $51 → $53.

Stock B jumps around wildly from $50 → $60 → $45 → $58.

Even with the same current price, Stock B’s options will cost more — because the potential for profit is bigger.🧠 Real-Life Analogy:

Imagine two friends:

One is calm and predictable (like Stock A).

The other is unpredictable — might surprise you big time (like Stock B).

Interest Rates: The Silent Factor (🏦)

Impact: Changes in interest rates have a relatively minor effect on most short-term stock options. They become more noticeable for long-term options (LEAPS).

Relationship:

Calls: Higher interest rates generally lead to slightly higher call premiums.

Puts: Higher interest rates generally lead to slightly lower put premiums.

Think: This is more complex, relating to the cost of holding or borrowing the underlying asset. For now, understand it's a minor factor for typical stock options.

Example:

If rates rise sharply, investors might prefer holding cash instead of buying stock, which slightly pushes Call prices up and Put prices down.

But this effect is minimal for short-term options (like 1–2 months).🧠 Real-Life Analogy:

Think of interest rates like the rent you pay for money.

When rent (interest) is higher, it costs more to own assets (like stocks), so calls get a small boost (since they delay buying), while puts lose a bit of appeal.

🧾 Summary Table

The 5 Key Factors and How They Affect Option Value (Premium)

🎯 Big Takeaway

These five forces work together — like gears in a machine — to shape every option’s price.

Once you understand them, you can predict how your option’s value might move as the market changes.

That’s how you move from guessing → to strategic thinking in options trading.