Section 6: Time Value and Its Decay (Theta θ)

Time Value and Its Decay (Theta θ)

11/13/20256 min read

The price you pay for an option is composed of two parts: Intrinsic Value (the option's immediate worth if exercised) and Extrinsic Value (the remaining value, which is essentially the Time Value and the value of volatility).

Extrinsic value is heavily dependent on how much time is left until an option expires. This brings us to one of the most important and fundamental concepts for options traders: Time Decay, often represented by the Greek letter Theta (θ).

The Ticking Clock: The Concept of Time Decay

The Concept: As each day passes and an option gets closer to its expiration date, its extrinsic (time) value naturally decreases. This loss of value, purely due to the passage of time, is called Time Decay. By expiration, the extrinsic value of any option is always zero.

Why it happens: The less time an option has, the less opportunity there is for the underlying stock to make a big move. The "potential" component of the option's value simply fades away.

💡 Life Analogy: The Concert Ticket Resale Value

Imagine you buy a non-refundable, transferable ticket to a highly anticipated concert happening 6 months from now.

High Time Value (6 months out): The resale value of your ticket is very high. Why? Because a lot can happen—the artist could release a new hit, driving up demand, or you have plenty of time to find a buyer. The time itself gives the ticket potential.

Low Time Value (1 day before): The day before the concert, the resale value is much lower (unless it's below face value). Your time to find a buyer and the possibility of a major market change (like a huge surge in demand) are minimal. The time value has almost completely decayed.

Zero Time Value (After the concert): Once the concert is over, the ticket is worthless. Its time value has vanished entirely.

Understanding Theta θ

Theta (θ): Theta is one of the "Greeks" (which we'll discuss more later) that quantifies this decay. It is typically expressed as a negative number.

The Measurement: A Theta of -0.05$ (or simply 0.05$) means the option's value is expected to decrease by 0.05$ per day, all else being equal (assuming no change in stock price or volatility).

💡 Life Analogy: Car Rental Insurance

Think of the time value as an insurance policy you buy against the stock not moving fast enough in your favor.

You rent a car for three days. The insurance you buy for those three days has value.

Theta is the daily cost of that insurance. Every morning you wake up, one day of your insurance is used up, and its remaining value decreases. The option premium is paying for a certain duration of market access, and Theta is the rate at which that duration costs you money.

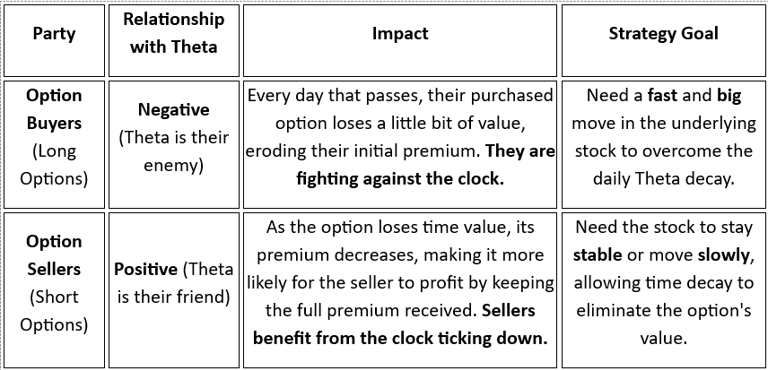

Impact on Buyers vs. Sellers

Time decay has opposite effects on options buyers and sellers, making it a crucial component of options strategy.

For Option Buyers (Long Options): Time decay is generally negative. Every day that passes, your purchased option loses a little bit of value, eroding your premium. You are fighting against the clock.

For Option Sellers (Short Options): Time decay is generally positive. As the option loses time value, its premium decreases, making it more likely for the seller to profit by keeping the premium received if the option expires worthless. Sellers benefit from the clock ticking down.

This is perhaps the most important detail to understand about Theta: Time decay is not linear.

The Reality: The loss of time value is slow and steady when an option has 90+ days to expiration, but it accelerates significantly in the last 30-45 days before expiration.

The Reason: Options lose value much faster as they get very close to expiring because the statistical probability of a major, market-altering event drops drastically in the final days. The "potential" is largely gone.

💡 Life Analogy: The Melting Ice Cube

Imagine an ice cube melting:

Slow Decay (90 days out): When the ice cube is large (far from expiration), it melts slowly. The difference between 90 days and 89 days is minor.

Accelerated Decay (30 days out): As the ice cube gets smaller (closer to expiration), it melts much faster. The difference between the last 5 minutes and the last 4 minutes is much more noticeable than the difference between the first hour and the second hour.

In options, the time value (extrinsic value) is the "ice." It melts slowly at first, but once you cross that threshold (around 30-45 days), the rate of melting (Theta decay) dramatically increases, rapidly sucking the remaining time value out of the option.

The price you pay for an option is composed of two parts: Intrinsic Value (the option's immediate worth if exercised) and Extrinsic Value (the remaining value, which is essentially the Time Value and the value of volatility).

Extrinsic value is heavily dependent on how much time is left until an option expires. This brings us to one of the most important and fundamental concepts for options traders: Time Decay, often represented by the Greek letter Theta.

The Ticking Clock: The Concept of Time Decay

The Concept: As each day passes and an option gets closer to its expiration date, its extrinsic (time) value naturally decreases. This loss of value, purely due to the passage of time, is called Time Decay. By expiration, the extrinsic value of any option is always zero.

Why it happens: The less time an option has, the less opportunity there is for the underlying stock to make a big move. The "potential" component of the option's value simply fades away.

💡 Life Analogy: The Concert Ticket Resale Value

Imagine you buy a non-refundable, transferable ticket to a highly anticipated concert happening 6 months from now.

High Time Value (6 months out): The resale value of your ticket is very high. Why? Because a lot can happen—the artist could release a new hit, driving up demand, or you have plenty of time to find a buyer. The time itself gives the ticket potential.

Low Time Value (1 day before): The day before the concert, the resale value is much lower (unless it's below face value). Your time to find a buyer and the possibility of a major market change (like a huge surge in demand) are minimal. The time value has almost completely decayed.

Zero Time Value (After the concert): Once the concert is over, the ticket is worthless. Its time value has vanished entirely.

Understanding Theta θ

Theta (θ): Theta is one of the "Greeks" (which we'll discuss more later) that quantifies this decay. It is typically expressed as a negative number.

The Measurement: A Theta of -0.05$ (or simply 0.05$) means the option's value is expected to decrease by 0.05$ per day, all else being equal (assuming no change in stock price or volatility).

💡 Life Analogy: Car Rental Insurance

Think of the time value as an insurance policy you buy against the stock not moving fast enough in your favor.

You rent a car for three days. The insurance you buy for those three days has value.

Theta is the daily cost of that insurance. Every morning you wake up, one day of your insurance is used up, and its remaining value decreases. The option premium is paying for a certain duration of market access, and Theta is the rate at which that duration costs you money.

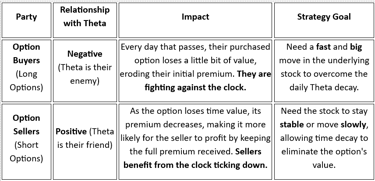

Impact on Buyers vs. Sellers

Time decay has opposite effects on options buyers and sellers, making it a crucial component of options strategy.

For Option Buyers (Long Options): Time decay is generally negative. Every day that passes, your purchased option loses a little bit of value, eroding your premium. You are fighting against the clock.

For Option Sellers (Short Options): Time decay is generally positive. As the option loses time value, its premium decreases, making it more likely for the seller to profit by keeping the premium received if the option expires worthless. Sellers benefit from the clock ticking down.

This is perhaps the most important detail to understand about Theta: Time decay is not linear.

The Reality: The loss of time value is slow and steady when an option has 90+ days to expiration, but it accelerates significantly in the last 30-45 days before expiration.

The Reason: Options lose value much faster as they get very close to expiring because the statistical probability of a major, market-altering event drops drastically in the final days. The "potential" is largely gone.

💡 Life Analogy: The Melting Ice Cube

Imagine an ice cube melting:

Slow Decay (90 days out): When the ice cube is large (far from expiration), it melts slowly. The difference between 90 days and 89 days is minor.

Accelerated Decay (30 days out): As the ice cube gets smaller (closer to expiration), it melts much faster. The difference between the last 5 minutes and the last 4 minutes is much more noticeable than the difference between the first hour and the second hour.

In options, the time value (extrinsic value) is the "ice." It melts slowly at first, but once you cross that threshold (around 30-45 days), the rate of melting (Theta decay) dramatically increases, rapidly sucking the remaining time value out of the option.