Section 9: Basic Options Strategies

Buying Calls and Puts - Selling covered calls - Protective puts

BEGINNER LEVEL

10/7/202512 min read

1. Buying calls and puts

Now that you understand what options are, how the market works, and how options are priced, it's time to learn some practical strategies. These are the building blocks of options trading, allowing you to participate in the market with defined goals and risk profiles.

We'll focus on three fundamental strategies: buying calls, buying puts, and selling covered calls.

1.1 Buying Calls: ُExpecting on an Upside Move (Long Call)

Buying a call option is the most straightforward way to use options to profit from a stock price increase. It's often used as an alternative to buying the stock outright, offering significant leverage.

What it is: You purchase a call option contract, giving you the right to buy 100 shares of the underlying stock at a specific strike price on or before the expiration date.

When to use it (Market View): You are bullish on the underlying stock. You believe its price will increase significantly (above the strike price) before the option expires.

Why use it over buying stock?

Leverage: You control 100 shares of stock for a much smaller capital outlay (the premium) than buying 100 shares directly. This means higher potential percentage returns if your prediction is correct.

Defined Risk: Your maximum loss is limited to the premium you pay for the option.

Risk and Reward Profile:

Maximum Risk: Limited to the premium paid (per contract).

Maximum Reward: Unlimited. As the stock price rises, the call option's intrinsic value increases, and it can theoretically go up indefinitely.

Break-Even Point: Strike Price + Premium Paid

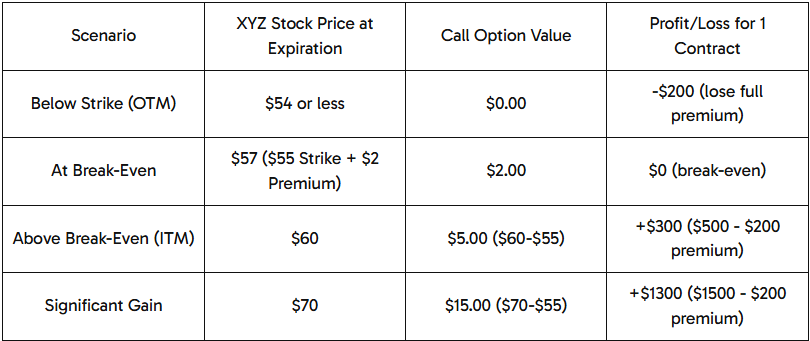

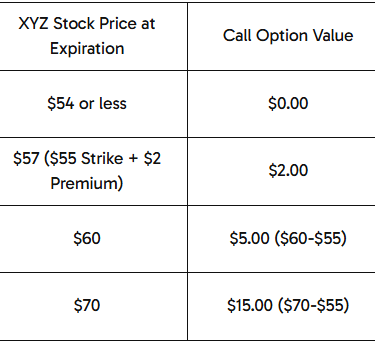

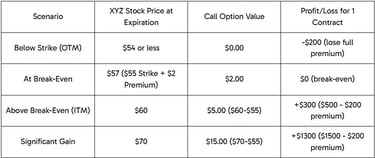

Example: Buying a Call Option

Let's say XYZ stock is currently trading at $50 per share. You are very bullish and expect it to go up significantly.

You buy 1 XYZ $55 Call option expiring in 3 months for a premium of $2.00 per share (total cost: $2.00 x 100 shares = $200).

Important Considerations for Buying Calls:

Time Decay: This is working against you. The stock needs to move up before the option loses too much time value.

Strike Price Choice: Choosing a higher strike (more OTM) means a lower premium but requires a larger move in the stock to become profitable. Choosing a lower strike (more ITM or ATM) means a higher premium but requires a smaller move.

1.2 Buying Puts: Expecting a Downside Move (Long Put)

Risk and Reward Profile:

Maximum Risk: Limited to the premium paid (per contract).

Maximum Reward: Substantial, as a stock can fall to $0 (though it's capped at the strike price minus premium paid).

Break-Even Point: Strike Price - Premium Paid

Example: Buying a Put Option

Let's say ABC stock is currently trading at $100 per share. You are bearish and expect it to drop.

You buy 1 ABC $95 Put option expiring in 3 months for a premium of $3.00 per share (total cost: $3.00 x 100 shares = $300).

Important Considerations for Buying Puts:

Time Decay: Just like calls, time decay works against put buyers. The stock needs to fall quickly enough.

Strike Price Choice: Similar to calls, a lower strike (more OTM) is cheaper but requires a larger drop. A higher strike (more ITM or ATM) is more expensive but requires a smaller drop to be profitable.

2. Selling Covered Calls: Generating Income (Covered Call)

Risk and Reward Profile:

Maximum Risk: The potential loss on your stock holdings if the stock price drops below your purchase price (minus the premium received). Your stock can still go to $0.

Maximum Reward: Limited to the premium received + (Strike Price - Stock Purchase Price). If the stock goes far above the strike, you miss out on further gains beyond the strike price, as your shares will be "called away" (exercised).

Break-Even Point: Stock Purchase Price - Premium Received

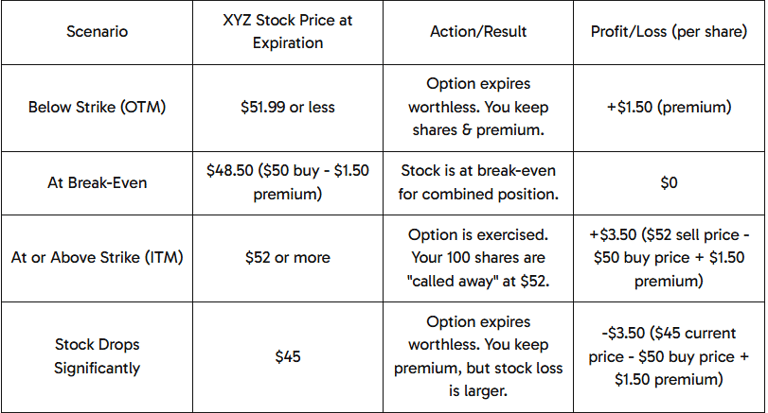

Example: Selling a Covered Call

Let's say you own 100 shares of XYZ stock that you bought at $50 per share. XYZ is currently trading at $50. You don't expect a huge move in the next month, but you're happy to collect some income.

You sell 1 XYZ $52 Call option expiring in 1 month for a premium of $1.50 per share (total collected: $1.50 x 100 shares = $150).

Selling a covered call is a popular strategy for income generation, often used by investors who already own the underlying stock. It's called "covered" because you own the shares to "cover" your obligation if the option is exercised.

What it is: You own at least 100 shares of a stock, and you sell (write) a call option against those shares. You collect the premium upfront.

When to use it (Market View): You are neutral to mildly bullish on the stock you own, or you don't mind selling your shares at the strike price if the stock goes up. You want to generate extra income from your existing stock holdings.

Why use it?

Income: You collect the premium immediately, which can enhance your returns or provide income in a sideways market.

Partial Downside Protection: The premium received offers a small buffer against a slight decline in the stock's price.

Important Considerations for Selling Covered Calls:

Opportunity Cost: You give up potential large gains if the stock skyrockets past your strike price. Your shares will be called away at the strike.

Time Decay: This is working for you. You want the option to lose time value and expire worthless so you keep the premium.

Selling NAKED Calls: Never to be confused with covered calls for beginners. Selling a call without owning the underlying stock is called a "naked call" and carries unlimited risk. This is generally not allowed for Level 1 or 2 options accounts and is highly risky.

3. Protective Puts: Your Insurance Policy (Long Put)

Risk and Reward Profile:

Maximum Risk: Limited to the cost of the put option (premium paid) + (Stock Purchase Price - Put Option Strike Price). Your total potential loss is capped at the difference between your purchase price and the strike price, plus the premium.

Maximum Reward: Unlimited upside on your stock, minus the cost of the put. If the stock goes up, you simply lose the premium paid for the put (your insurance cost).

Break-Even Point: Stock Purchase Price + Premium Paid

Example: Buying a Protective Put

Let's say you own 100 shares of XYZ stock that you bought at $50 per share. XYZ is currently trading at $50. You believe in XYZ long-term, but you're worried about a potential dip next month due to an upcoming announcement.

You buy 1 XYZ $45 Put option expiring in 1 month for a premium of $2.00 per share (total cost: $2.00 x 100 shares = $200).

Buying a protective put is a hedging strategy that allows you to protect the value of a stock you own from a significant downside move, similar to buying an insurance policy.

What it is: You own at least 100 shares of a stock, and you buy a put option on that same stock.

When to use it (Market View): You are bullish on the long-term prospects of a stock you own, but you are bearish or uncertain about its short-term performance. You want to limit your potential loss on your stock holding without selling the shares.

Why use it?

Defined Downside Protection: It sets a "floor" on your potential losses for the covered shares.

Flexibility: You retain your stock ownership and potential upside if the stock does not fall.

Capital Preservation: Helps protect your capital during volatile periods.

Buying a put option is the primary way to use options to profit from a falling stock price. It's often used for speculation or as an "insurance policy" for stocks you own (which we'll discuss next).

What it is: You purchase a put option contract, giving you the right to sell 100 shares of the underlying stock at a specific strike price on or before the expiration date.

When to use it (Market View): You are bearish on the underlying stock. You believe its price will decrease significantly (below the strike price) before the option expires.

Why use it over Short Selling Stock?

Defined Risk: Your maximum loss is limited to the premium you pay for the option. This is a huge advantage over short selling stock, which has theoretically unlimited risk.

Leverage: Similar to calls, you control 100 shares for a smaller upfront cost.

Important Considerations for Protective Puts:

Cost of Protection: The premium you pay for the put is an expense that reduces your overall return on the stock if it doesn't fall.

Time Decay: This is working against you, as the put option will lose value as time passes if the stock doesn't drop.

Strike Choice: A higher strike put offers more protection but costs more. A lower strike put offers less protection but costs less.

These three basic strategies form the bedrock of options trading. Practice understanding their mechanics, their risk/reward profiles, and when each is appropriate.

1. Buying calls and puts

Now that you understand what options are, how the market works, and how options are priced, it's time to learn some practical strategies. These are the building blocks of options trading, allowing you to participate in the market with defined goals and risk profiles.

We'll focus on three fundamental strategies: buying calls, buying puts, and selling covered calls.

1.1 Buying Calls: ُExpecting on an Upside Move (Long Call)

Buying a call option is the most straightforward way to use options to profit from a stock price increase. It's often used as an alternative to buying the stock outright, offering significant leverage.

What it is: You purchase a call option contract, giving you the right to buy 100 shares of the underlying stock at a specific strike price on or before the expiration date.

When to use it (Market View): You are bullish on the underlying stock. You believe its price will increase significantly (above the strike price) before the option expires.

Why use it over buying stock?

Leverage: You control 100 shares of stock for a much smaller capital outlay (the premium) than buying 100 shares directly. This means higher potential percentage returns if your prediction is correct.

Defined Risk: Your maximum loss is limited to the premium you pay for the option.

Risk and Reward Profile:

Maximum Risk: Limited to the premium paid (per contract).

Maximum Reward: Unlimited. As the stock price rises, the call option's intrinsic value increases, and it can theoretically go up indefinitely.

Break-Even Point: Strike Price + Premium Paid

Example: Buying a Call Option

Let's say XYZ stock is currently trading at $50 per share. You are very bullish and expect it to go up significantly.

You buy 1 XYZ $55 Call option expiring in 3 months for a premium of $2.00 per share (total cost: $2.00 x 100 shares = $200).

1.2 Buying Puts: Expecting a Downside Move (Long Put)

Risk and Reward Profile:

Maximum Risk: Limited to the premium paid (per contract).

Maximum Reward: Substantial, as a stock can fall to $0 (though it's capped at the strike price minus premium paid).

Break-Even Point: Strike Price - Premium Paid

Example: Buying a Put Option

Let's say ABC stock is currently trading at $100 per share. You are bearish and expect it to drop.

You buy 1 ABC $95 Put option expiring in 3 months for a premium of $3.00 per share (total cost: $3.00 x 100 shares = $300).

Important Considerations for Buying Puts:

Time Decay: Just like calls, time decay works against put buyers. The stock needs to fall quickly enough.

Strike Price Choice: Similar to calls, a lower strike (more OTM) is cheaper but requires a larger drop. A higher strike (more ITM or ATM) is more expensive but requires a smaller drop to be profitable.

2. Selling Covered Calls: Generating Income (Covered Call)

Risk and Reward Profile:

Maximum Risk: The potential loss on your stock holdings if the stock price drops below your purchase price (minus the premium received). Your stock can still go to $0.

Maximum Reward: Limited to the premium received + (Strike Price - Stock Purchase Price). If the stock goes far above the strike, you miss out on further gains beyond the strike price, as your shares will be "called away" (exercised).

Break-Even Point: Stock Purchase Price - Premium Received

Example: Selling a Covered Call

Let's say you own 100 shares of XYZ stock that you bought at $50 per share. XYZ is currently trading at $50. You don't expect a huge move in the next month, but you're happy to collect some income.

You sell 1 XYZ $52 Call option expiring in 1 month for a premium of $1.50 per share (total collected: $1.50 x 100 shares = $150).

Selling a covered call is a popular strategy for income generation, often used by investors who already own the underlying stock. It's called "covered" because you own the shares to "cover" your obligation if the option is exercised.

What it is: You own at least 100 shares of a stock, and you sell (write) a call option against those shares. You collect the premium upfront.

When to use it (Market View): You are neutral to mildly bullish on the stock you own, or you don't mind selling your shares at the strike price if the stock goes up. You want to generate extra income from your existing stock holdings.

Why use it?

Income: You collect the premium immediately, which can enhance your returns or provide income in a sideways market.

Partial Downside Protection: The premium received offers a small buffer against a slight decline in the stock's price.

Important Considerations for Selling Covered Calls:

Opportunity Cost: You give up potential large gains if the stock skyrockets past your strike price. Your shares will be called away at the strike.

Time Decay: This is working for you. You want the option to lose time value and expire worthless so you keep the premium.

Selling NAKED Calls: Never to be confused with covered calls for beginners. Selling a call without owning the underlying stock is called a "naked call" and carries unlimited risk. This is generally not allowed for Level 1 or 2 options accounts and is highly risky.

3. Protective Puts: Your Insurance Policy (Long Put)

Risk and Reward Profile:

Maximum Risk: Limited to the cost of the put option (premium paid) + (Stock Purchase Price - Put Option Strike Price). Your total potential loss is capped at the difference between your purchase price and the strike price, plus the premium.

Maximum Reward: Unlimited upside on your stock, minus the cost of the put. If the stock goes up, you simply lose the premium paid for the put (your insurance cost).

Break-Even Point: Stock Purchase Price + Premium Paid

Example: Buying a Protective Put

Let's say you own 100 shares of XYZ stock that you bought at $50 per share. XYZ is currently trading at $50. You believe in XYZ long-term, but you're worried about a potential dip next month due to an upcoming announcement.

You buy 1 XYZ $45 Put option expiring in 1 month for a premium of $2.00 per share (total cost: $2.00 x 100 shares = $200).

Buying a protective put is a hedging strategy that allows you to protect the value of a stock you own from a significant downside move, similar to buying an insurance policy.

What it is: You own at least 100 shares of a stock, and you buy a put option on that same stock.

When to use it (Market View): You are bullish on the long-term prospects of a stock you own, but you are bearish or uncertain about its short-term performance. You want to limit your potential loss on your stock holding without selling the shares.

Why use it?

Defined Downside Protection: It sets a "floor" on your potential losses for the covered shares.

Flexibility: You retain your stock ownership and potential upside if the stock does not fall.

Capital Preservation: Helps protect your capital during volatile periods.

Buying a put option is the primary way to use options to profit from a falling stock price. It's often used for speculation or as an "insurance policy" for stocks you own (which we'll discuss next).

What it is: You purchase a put option contract, giving you the right to sell 100 shares of the underlying stock at a specific strike price on or before the expiration date.

When to use it (Market View): You are bearish on the underlying stock. You believe its price will decrease significantly (below the strike price) before the option expires.

Why use it over Short Selling Stock?

Defined Risk: Your maximum loss is limited to the premium you pay for the option. This is a huge advantage over short selling stock, which has theoretically unlimited risk.

Leverage: Similar to calls, you control 100 shares for a smaller upfront cost.

Important Considerations for Protective Puts:

Cost of Protection: The premium you pay for the put is an expense that reduces your overall return on the stock if it doesn't fall.

Time Decay: This is working against you, as the put option will lose value as time passes if the stock doesn't drop.

Strike Choice: A higher strike put offers more protection but costs more. A lower strike put offers less protection but costs less.

These three basic strategies form the bedrock of options trading. Practice understanding their mechanics, their risk/reward profiles, and when each is appropriate.

Important Considerations for Buying Calls:

Time Decay: This is working against you. The stock needs to move up before the option loses too much time value.

Strike Price Choice: Choosing a higher strike (more OTM) means a lower premium but requires a larger move in the stock to become profitable. Choosing a lower strike (more ITM or ATM) means a higher premium but requires a smaller move.